Listed REITs are a liquid investment in income-producing real estate that have historically delivered positive total returns and a high dividend yield that is attractive to investors seeking income from their portfolio. Investing in REITs can help reduce the volatility of a portfolio’s returns, as they have relatively low correlations with other asset classes.

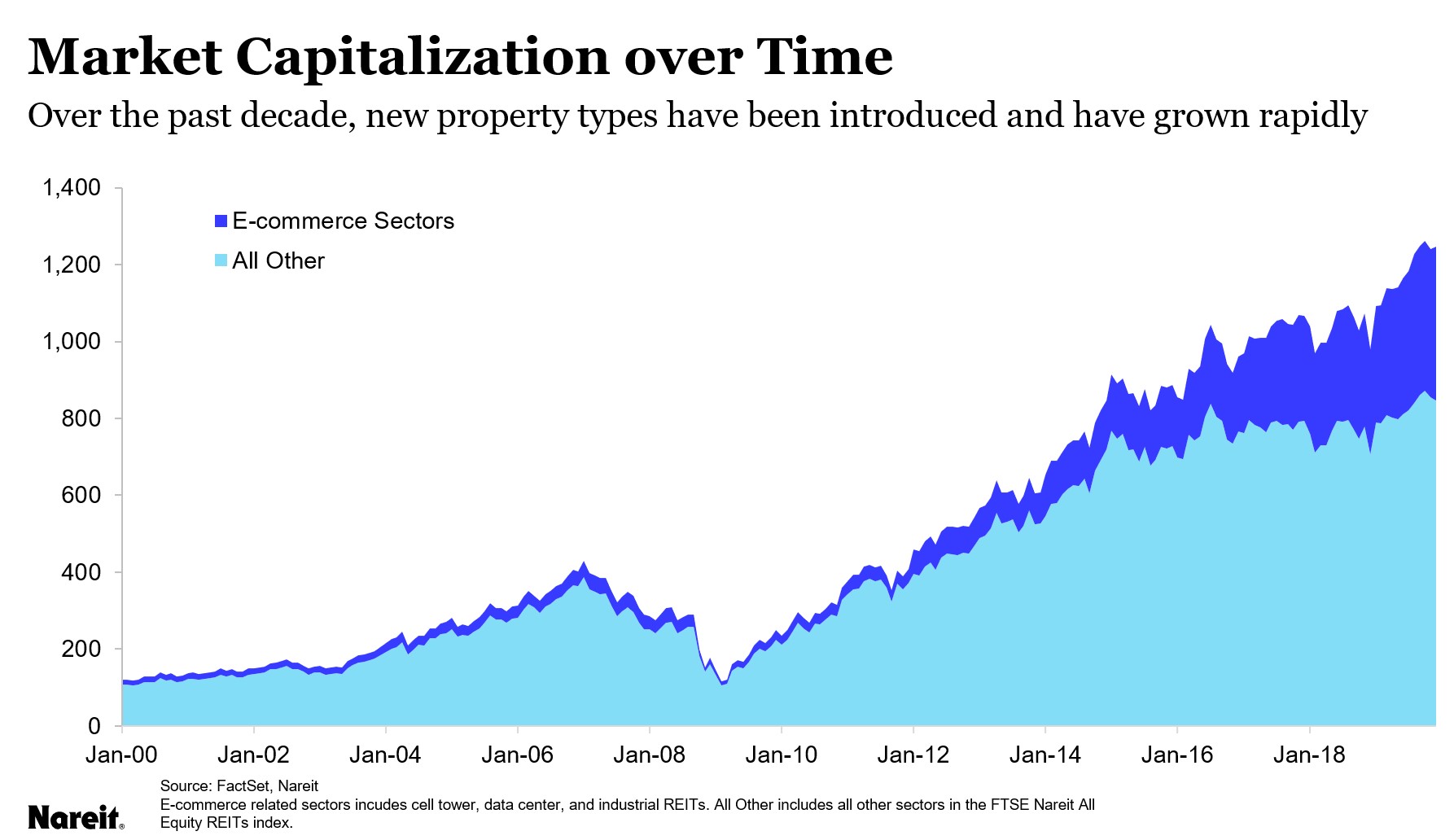

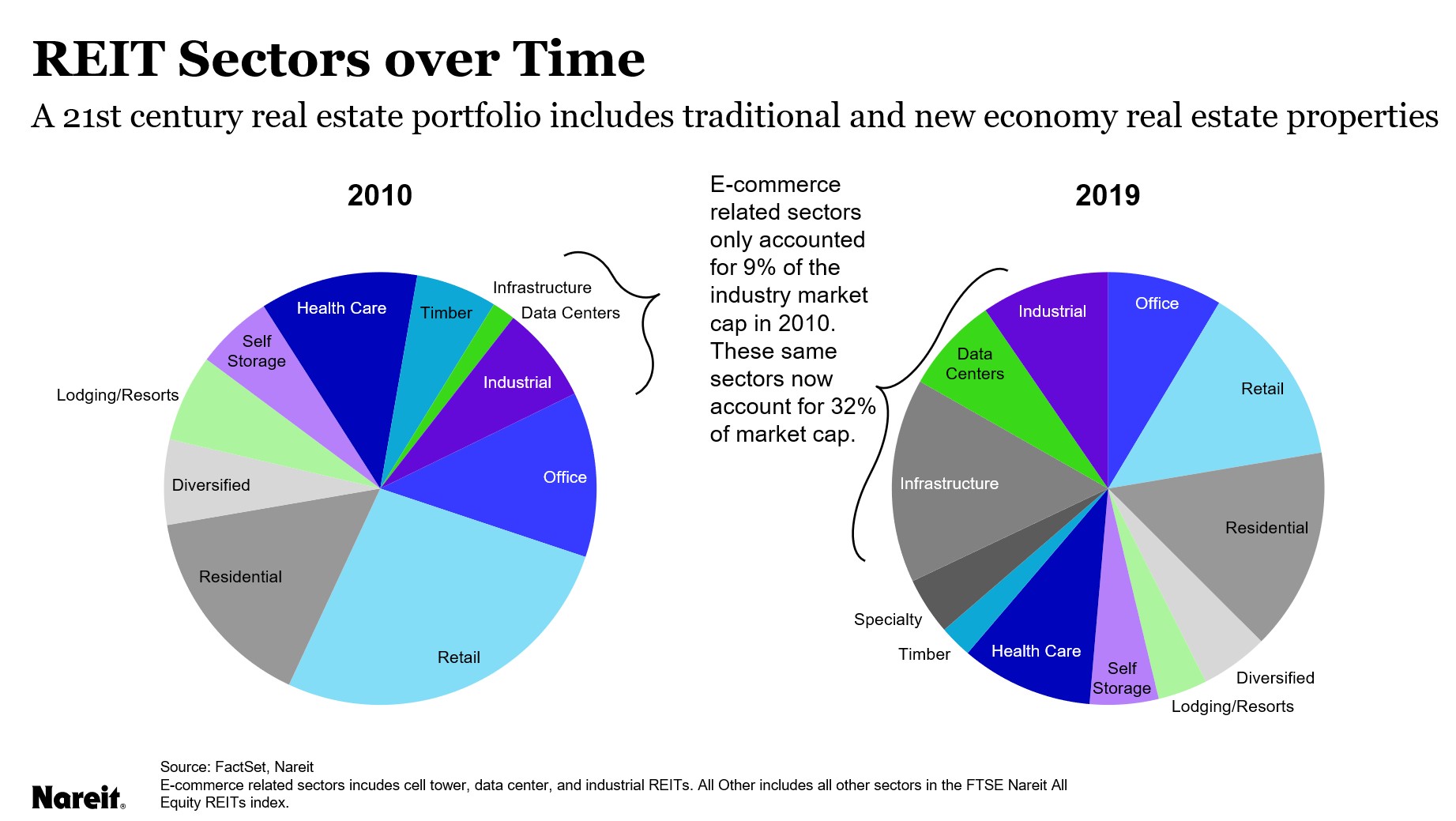

The growth and evolution of the REIT sector has given rise to an important new dimension of portfolio diversification. The REIT universe has expanded greatly beyond the property sectors institutional investors traditionally owned—Retail, Office, Residential and Industrial (RORI). In 2000, these sectors comprised over 75% of the market capitalization of equity REITs. Over the past decade, new property types have been introduced and have grown rapidly. Today, these property types outside of RORI account for half of total market capitalization.

Of special interest are REITs that invest in real estate that supports the rapidly growing technology sectors of the global economy.

New economy and high-tech real estate

Technology has changed nearly every aspect of the U.S. and the global economy. Two of the most prominent areas are the spread of internet communications and the rise of e-commerce. According to Cisco, global internet traffic has expanded ten-fold since 2010 and is projected to continue this pace of exponential growth. E-commerce has nearly tripled over this period, rising much more rapidly than in-store sales.

The common adage, “real estate houses the economy,” applies to the new tech economy, as well. Internet communications and e-commerce both depend on tech-related real estate, and REITs are active in owning and developing real estate that supports the tech economy. In particular, the Infrastructure sector includes REITs that own cell towers that transmit voice and data messages, and the Data Center REITs provide the facilities that house the servers that help link the data communications, store data and maintain internet web sites. These sectors now account for 23% of the market capitalization of all equity REITs, and other new and emerging sectors account for an additional 10% of total market capitalization. In the Industrial sector of the REIT industry, logistics space has overtaken traditional warehouse and flex space as the dominant form of industrial real estate. Logistics facilities are essential for the rapid delivery of goods bought via e-commerce.

The diversity of REIT property sectors can translate directly into improved diversification for the investor who holds not only traditional property types of RORI but also the newer REIT property types. Total investment returns range widely, with Infrastructure, Industrial and Data Center REITs delivering annualized total returns of nearly 20% since 2014 (Source: Nareit analysis of FTSE Nareit All Equity REITs Index as of December 2019).

Returns of different REIT sectors do not typically move in lock-step with one another, especially among the newer property types, so incorporating the newer property types into a portfolio can provide additional diversification and reduced risks. The correlation between the traditional RORI property types (Retail Office, Residential and Industrial) and the tech-related REIT types, Infrastructure and Data Centers is 47%. This low correlation between the traditional RORI property types and the tech sectors means combining the property types can yield significant diversification benefits.

Completion portfolios

A portfolio that holds assets and property types in the same proportions as a decade ago would miss out on the diversification that can be achieved by investing in these newer and more rapidly growing REIT types. One idea is to use REITs to create a “completion portfolio” that consists of these new sectors to complement the traditional real estate types in order to achieve more robust diversification.

Consider the impact of including a completion portfolio of tech- related REIT types to a traditional RORI portfolio. The chart below shows the impact of adding these sectors to a core portfolio of RORI REITs for the five-year period 2014 through December 2019. Total return on the RORI portfolio was an annualized 10.5% over this period. A completion portfolio consisting of the Infrastructure and Data Center REITs, however, provided a total return of 18.9% over this period. The combined portfolio of RORI plus the completion portfolio, with each weighted by market capitalization, yielded 13.2%.

It is important to consider the impact of adding these new sectors on the volatility of the portfolio. The standard deviation of monthly returns on the RORI portfolio was 13.8% over this period. Returns on the completion portfolio consisting of Infrastructure and Data Center REITs were more volatile, however, with a standard deviation of 14.7%. Yet somewhat surprisingly, the monthly volatility of the combined portfolio decreased to 12.8%.