Nareit tracks quarterly investment holdings for the 27 largest actively managed real estate investment funds focusing on REIT investment for insight on expert investor sentiment. (Please note though that five funds had not reported second quarter data for this analysis.)

In the second quarter of 2024, active managers increased allocations in the digital sectors and health care. The data centers sector is the most overweight relative to its index weight in the funds, invested at 123% of its index share. Telecommunications had the largest year-over-year increase, up 2.7 percentage points and surpassing retail as the sector with the second highest share of actively managed assets. Health care’s quarterly increase of 1.8 percentage points in the second quarter jumped the sector into the third highest share of assets, its highest rank since the beginning of the series in 2010.

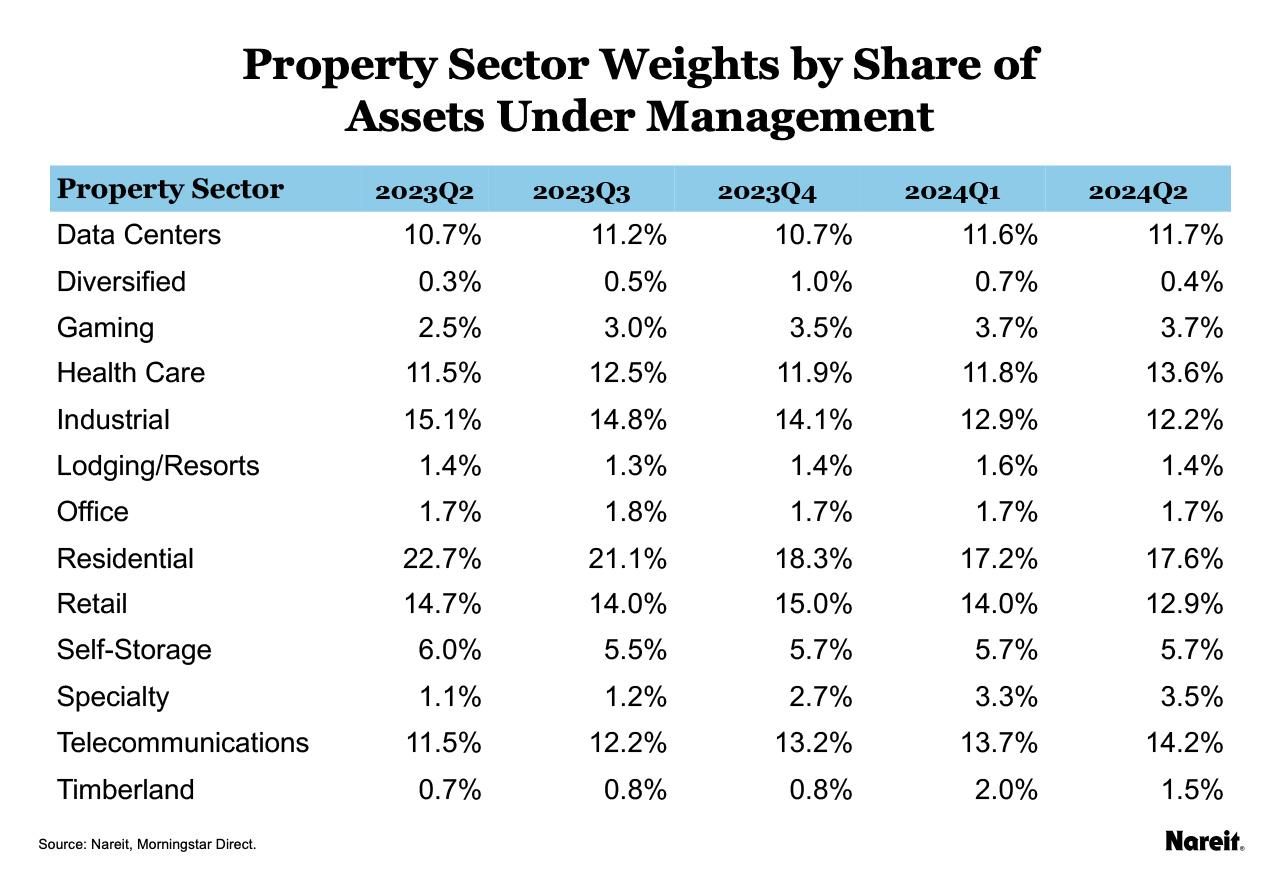

The table above shows the share of each equity REIT property sector by assets under management.

- Residential remains the property sector with the highest investment at 17.6%, followed by telecommunications at 14.2%.

- Health care has the third highest allocation at 13.6%—its highest rank since 2010. This drops retail and industrial down to fourth and fifth highest allocations respectively, at 12.9% and 12.2%, closely followed by data centers at 11.7%.

- Office, timberlands, and lodging/resorts are all less than 2%, with diversified less than 1%.

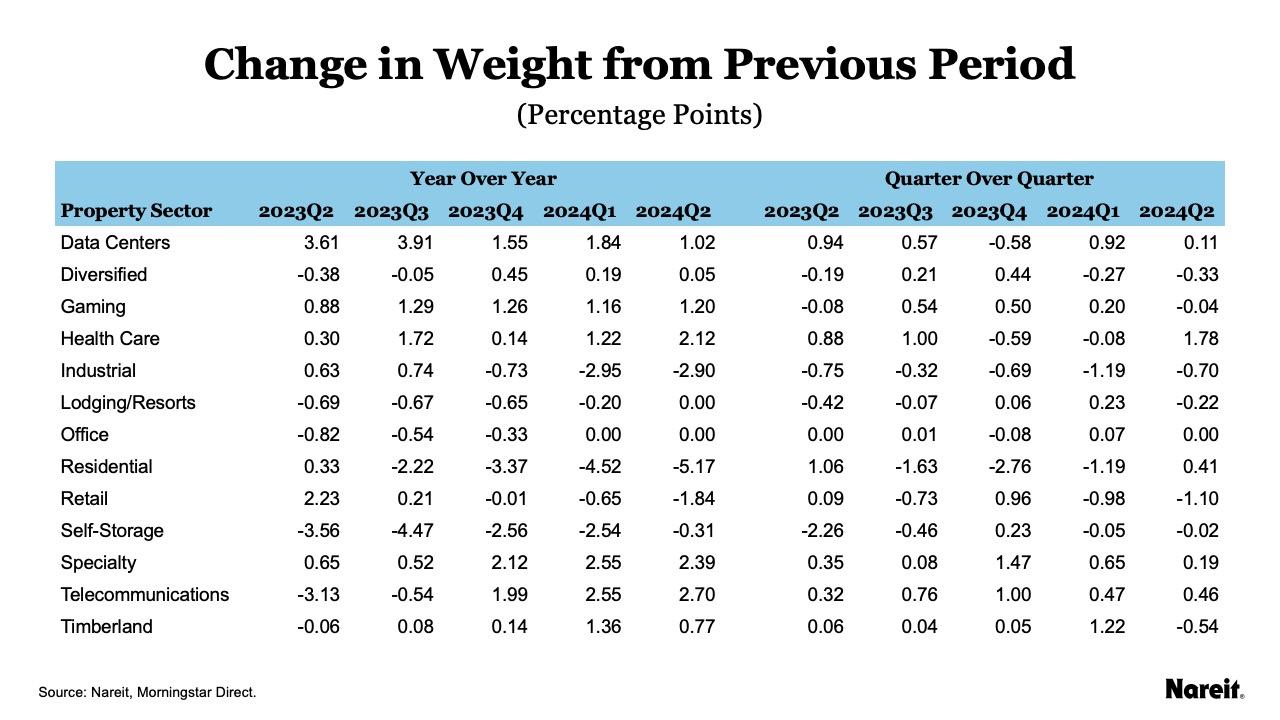

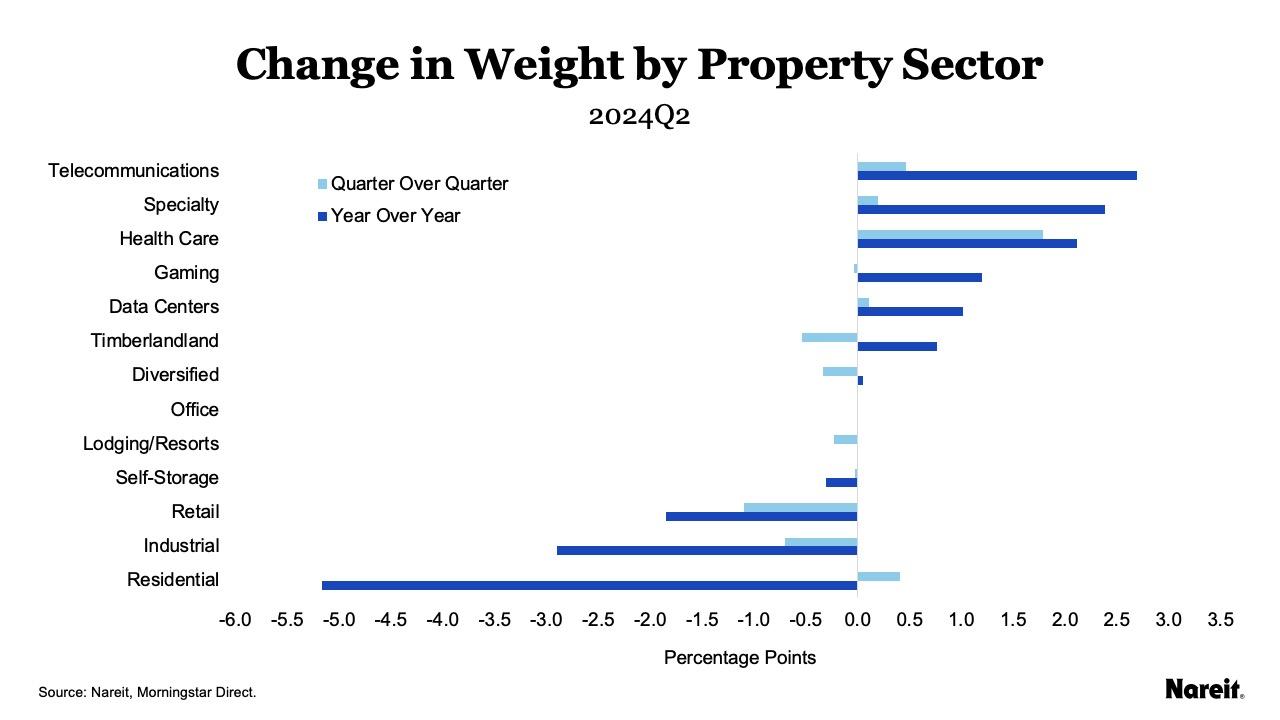

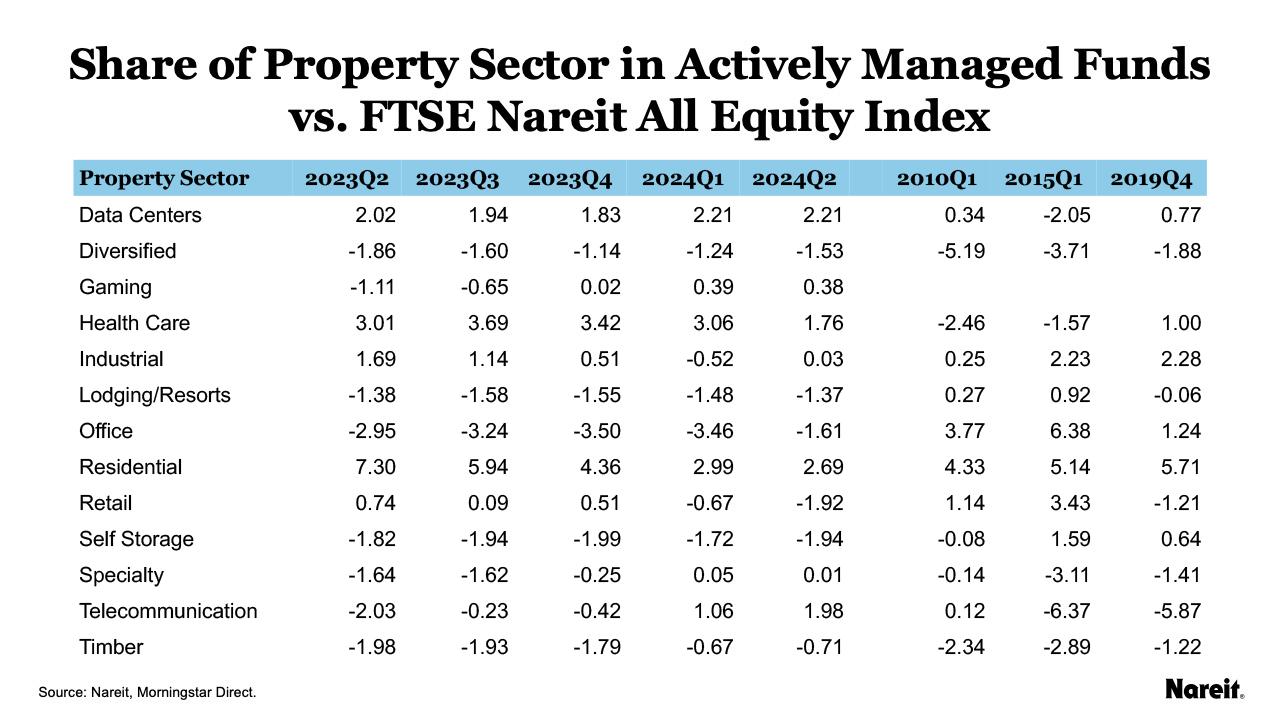

The table and chart above show the change in property sector asset share, by quarter and also from the previous year.

- Telecommunications continued to have the highest year-over-year gain in weight in 2024. The sector was up 2.7 percentage points year-over-year in the second quarter. The quarterly gain of 0.46 percentage points was also among the highest.

- Health care had the largest quarterly increase from Q1 2024, up 1.8 percentage points in the second quarter, allowing the sector to overtake retail and industrial for the third largest sector by assets under management. The sector had the third highest year-over-year weight change at 2.1 percentage points.

- Specialty was up modestly for the quarter at 0.19 percentage points but had the second highest increase from the previous year at 2.4 percentage points.

- Residential was up 0.41 percentage points quarter-over-quarter after three consecutive quarterly decreases. Despite the latest increase, the sector has the largest year-over-year decline, down 5.2 percentage points.

- Office, lodging/resorts, and diversified maintained their allocations for the year, all within 0.05 of the previous year’s share.

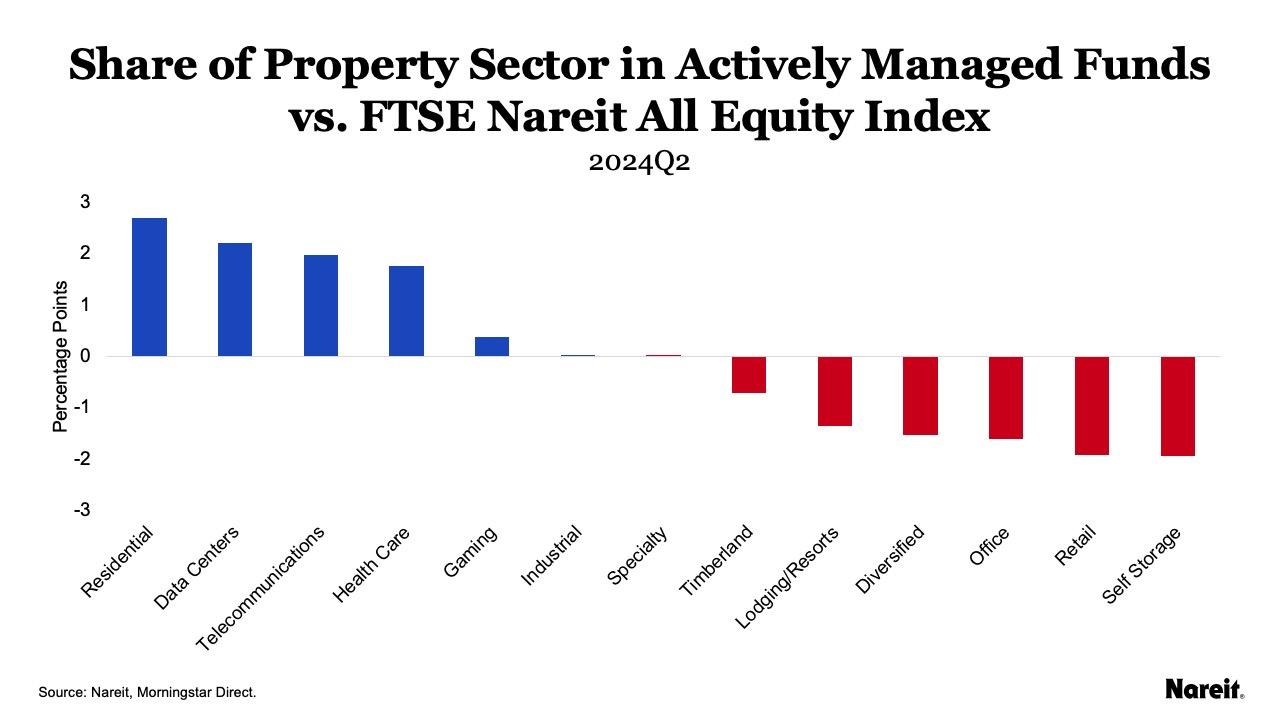

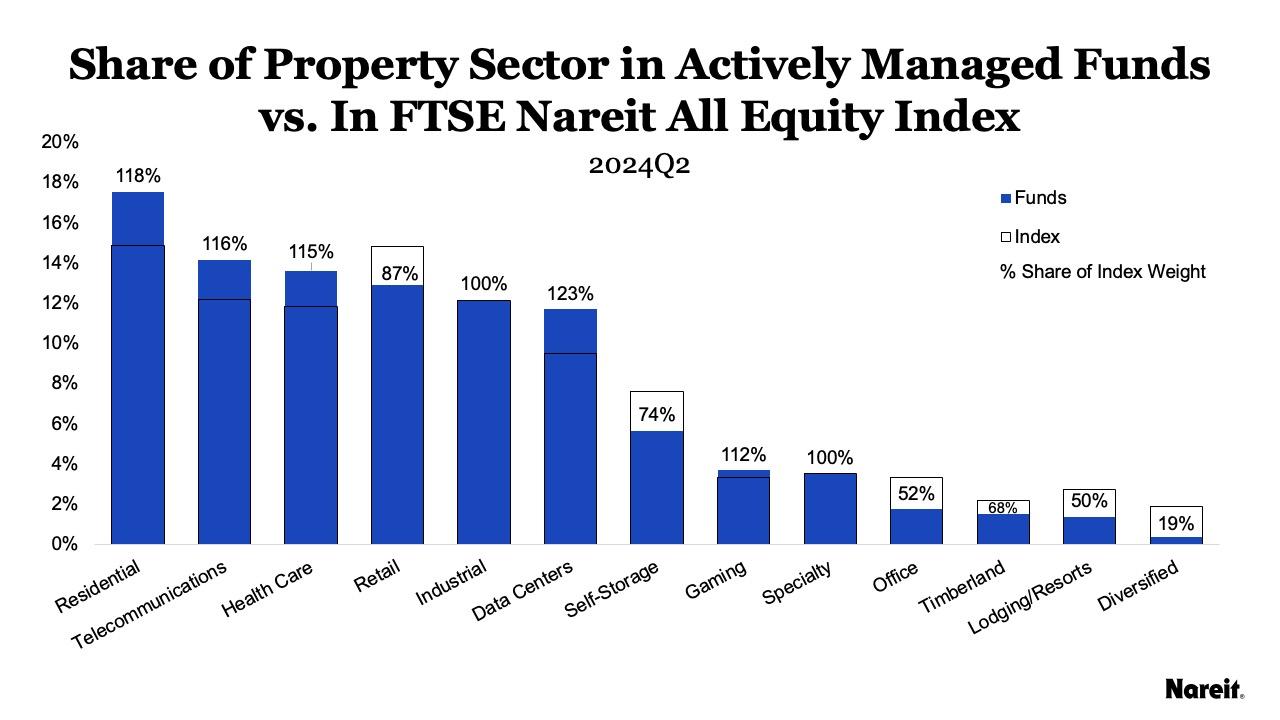

The charts and table above compare the weight of the sectors in actively managed funds to the weight of the sectors in the All Equity index.

- Funds are strongly overweight in digital sectors for Q2 2024. Data centers had the largest share relative to its index weight last quarter, for the first time surpassing residential. In Q2 2024, data centers continued to have the largest share relative to its index weight at 123%, or 2.2 percentage points over its index weight, and telecommunications was the third highest with an overweight share of 116%, or 2.0 percentage points.

- Residential’s large overweight in the funds has been steadily decreasing, going from 7.3 percentage points overweight (compared to the index in Q2 2023) down to 2.7 percentage points overweight in Q2 2024. Funds are invested at 118% of the index weight in residential.

- Health care is just behind telecommunications with an overweight share of its index weight at 115%. The sector is overweight compared to the index by 1.8 percentage points, even as its index weight has increased from 8.5% in Q2 2023 to 11.8% in Q2 2024.

- Retail’s share has continued to drop in Q2 2024 at 87% of index share.

- Industrial and specialty are near parity with their index weights. Industrial was overweight in 2023 and has declined to 0.03 percentage points overweight; while specialty was underweight and has increased to 0.01 percentage points overweight.

- Office, lodging/resorts, and diversified are the most underweight sectors.

- Diversified is the most underweight sector with just 19% of its index share, translating to 1.53 percentage points underweight.

- Lodging/resorts is also significantly underweight at 50% of its index share. The sector has been hovering around 1.5 percentage points underweight for the past year.

- With fund managers holding steady on their office weight the past two quarters, the sector has reduced its underweight (versus the index) as the index weight has fallen. Office is down to 3% of the index, and office is at 52% of its index share in Q2 2024, up from 34% in Q1.

For more information on the active manager project, see: Reading the Real Estate Market: Tracking Active Managers’ Allocations Over Time.