Retailers have long been adept at catering to consumers’ desires to get more for less. In the mid-1960s, Kmart started its Blue Light Specials. These seemingly impromptu, limited-time, in-store sales could be found by their hallmark flashing blue light and started with an announcement over the store intercom that said: “Attention Kmart shoppers.” Retailers have continued their efforts to entice consumers with regularly scheduled sales and Black Friday events; even Amazon has its Prime Days.

Just as consumers love bargains, investors also appreciate great values. While not advertised, investment buying opportunities do present themselves from time to time.

Today, U.S. public equity REITs appear to offer such a buying opportunity. REITs provide investors access to well-located, high-quality, institutional-grade properties managed by best-in-class operators. Recent data from the Nareit Total REIT Industry Tracker Series® (T-Tracker) and National Council of Real Estate Investment Fiduciaries (NCREIF) show that, on average, REITs have maintained higher occupancy rates than their private real estate counterparts across the four traditional property types. REITs also continued to remain attractively priced compared to private real estate. In the real estate space, REITs currently seem to offer more for less.

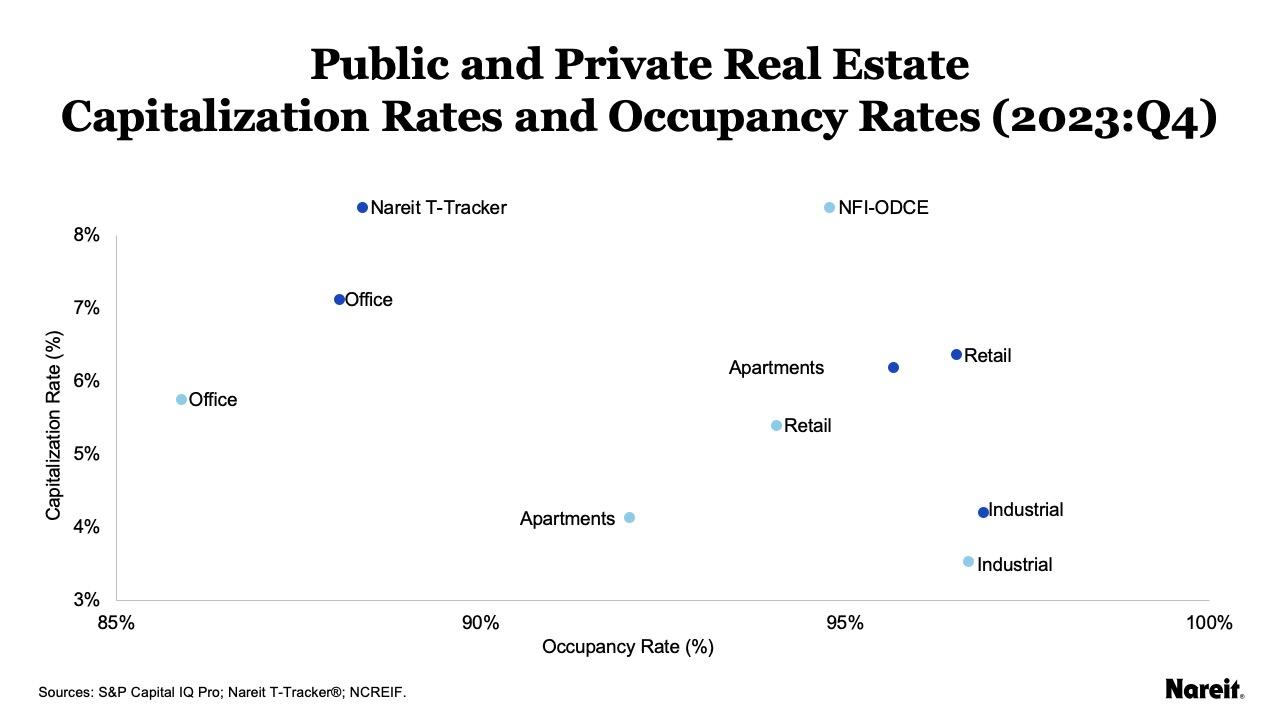

The chart above displays a scatter plot of public and private real estate capitalization (cap) rates and occupancy rates for the four traditional property types—apartments, industrial, office, and retail—as of the fourth quarter of 2023. Data from Nareit’s T-Tracker and NCREIF are used for the public and private real estate measures, respectively. The NCREIF data solely focus on properties from Open End Diversified Core Equity (ODCE) funds. The T-Tracker REIT implied and NCREIF appraisal cap rates used for the valuation metrics are calculated using backward-looking net operating incomes (NOIs).

A review of the chart shows that REIT occupancy rates exceeded their respective NCREIF ODCE occupancy rate counterparts across all the examined property types. Focusing on the differences between public and private real estate occupancy rates, apartments had the largest differential; it was 3.6%. The occupancy rate differences for the retail and office sectors were 2.5% and 2.2%, respectively. The industrial gap was the lowest at 0.2%. The higher REIT occupancy rates may simply be a function of operational focus. They may also be related to better asset management and/or property selection.

REIT implied cap rates also exceeded their respective NCREIF ODCE appraisal cap rates. In the fourth quarter of 2023, the public-private cap rate spreads were 206, 137, 96, and 67 basis points for the apartment, office, retail, and industrial sectors, respectively. All else equal, these significant spreads suggest that REITs offer more attractive pricing relative to private real estate across each of the examined property types. Pricing in some sectors like apartments remains particularly compelling.

Across the four traditional property types, U.S. public equity REITs have enjoyed better occupancy rates than their private real estate counterparts. REITs have also continued to maintain a pricing advantage. The combination of these factors presents a potential buying opportunity, especially for investors who appreciate good value. Borrowing from a bit from retail nostalgia, an apropos headline for the current real estate environment might be: “Attention real estate investors: REITs may offer more for less.”