Nearing the end of the earnings season, the impacts of COVID-19 and social distancing on commercial real estate during the second quarter are coming into view. Revenues, rent payments, and quarterly earnings declined sharply for hotels and retail. Digital communication and e-commerce commercial real estate thrived.

Looking ahead, assessing risks and opportunities in commercial real estate depends on the shape and timing of the post-COVID-19 world, and whether changes to consumer and renter behavior are transient or permanent. Short-term earnings and operating performance may be indicative of long-term trends, or may be crisis-only impacts.

The pandemic struck early and hard, with the FTSE Nareit All Equity REITs Index down 7.0% in February and down 18.7% by the end of March. However, the most recent months have shown modest increases, with total returns since March up 17.6%.

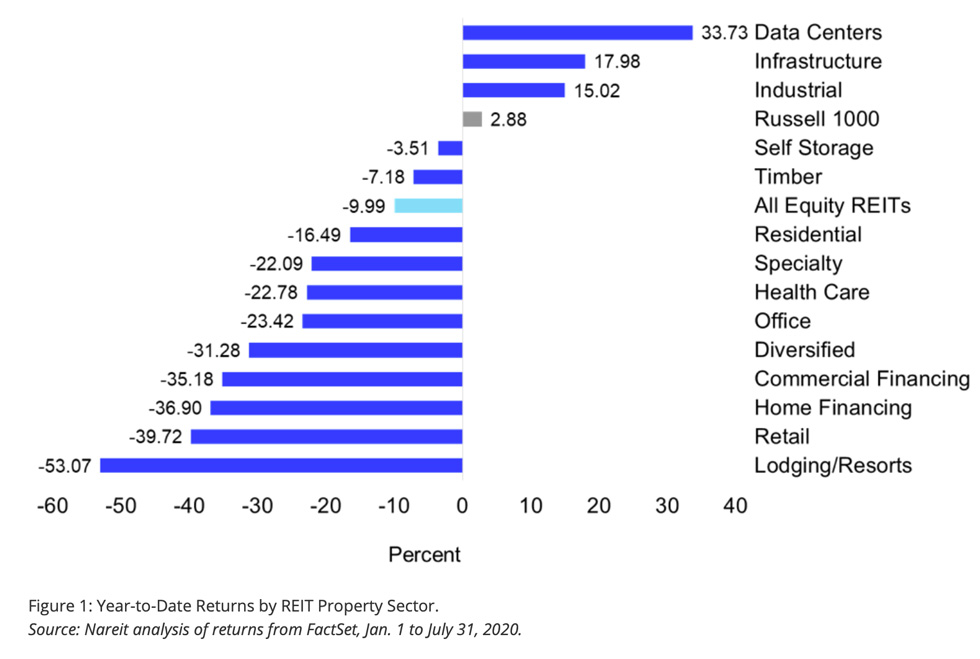

Separating REITs by property sector, as shown in Figure 1, paints a different picture of the pandemic’s impact on the industry. Year-to-date total returns for the FTSE Nareit All Equity REITs Index show the three sectors with the most exposure to e-commerce outperforming the rest of the index, as well as the broader Russell 1000 index. These sectors, comprised of cell phone towers (infrastructure), data centers, and industrial and logistics REITs, are sometimes referred to as 21st Century Real Estate. These sectors have grown from less than 10% of REIT equity market capitalization in 2010 to over 40% today. The COVID-19 crisis has increased demand for these property types, as more households shift their activities online, and the short-term impact has been positive for sectors already trending upward.

Considering the other major REIT sectors, retail and lodging/resorts are the hardest hit sectors, with year-to-date returns of –39.7% and –53.1%, respectively. These two sectors are the most directly affected by closures and social distancing. Office, healthcare, and residential are in the middle of the pack, with year-to-date returns of –23.4%, –22.6%, and –16.5%, respectively. The short-term impact is not as severe for these sectors, but neither are they immune from economy-wide trends.

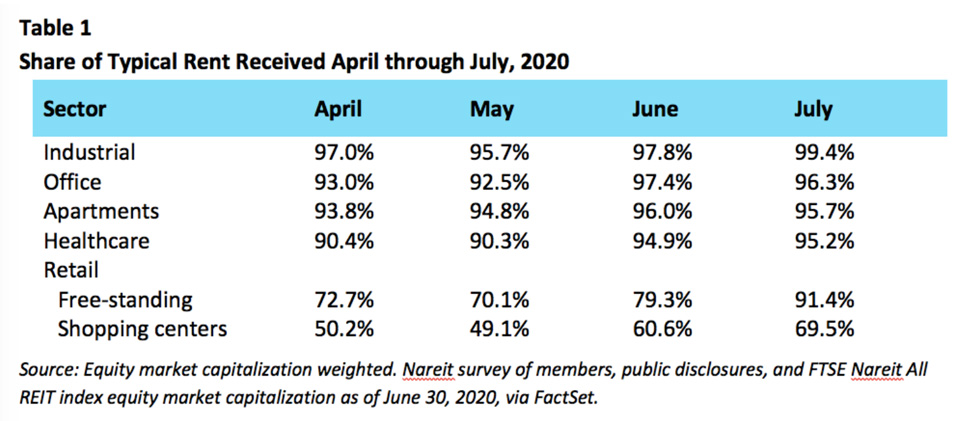

Turning to a more direct measure of operating performance, the results of Nareit’s monthly rent survey are summarized in Table 1.

The July results showed the industrial sector as the strongest performer, with collections consistently averaging above 95% of typical rents and rising to over 99% of typical rents in July. Importantly, the office, apartment, and healthcare sectors have all performed well, with collections above 90% of typical rents as tenants have reliably paid. Collections in these three sectors rose when the economy began reopening in June and July, compared with April and May.

Retail has been the hardest-hit sector in terms of rent collections, but there have been significant improvements over the past two months as many retailers have reopened and retail sales have rebounded. Free-standing retail made substantial gains in rent collections in July, up over 12 percentage points to 91%. Shopping center REITs continued to make gains in July, with up to 69% of rent collected.

Taken together, market returns and rent collections are not in complete agreement. Figure 2 brings together operational and market performance, dividing the industry into three categories to highlight the sectors affected most by the pandemic and its economic effects.

- Neutral or positive returns and operating performance, in dark blue, represents 54% of REIT equity market capitalization. These sectors are generally social-distancing friendly—data centers, infrastructure (cell phone towers), and industrial. The other sectors in this group are single family rentals, manufactured homes, and self-storage. Not only is the pandemic not leading to direct shutdowns, longer-term trends have generally been favoring these sectors.

- Negative returns and operating performance, in grey, represents 33% of REIT equity market capitalization. These sectors are generally in-person activities and retail. As discussed above, retail rent collections dropped precipitously in the early months of the crisis. While rent collections are recovering, significant debate surrounds whether and if consumers will fully return to retail shopping. The other sectors—diversified and specialty REITs—include retail properties and other experiential properties like casinos and amusement parks.

- Negative returns with neutral operating performance, in light blue, represents 18% of REIT equity market capitalization. These sectors have relatively strong operating performance in terms of rent collections, but also harbor concerns about long-run performance.

- The healthcare property sector is a mix of senior residential properties and medical facilities, including hospitals and medical office buildings. While rent payments have held up, senior residential facilities’ occupancy has started to fall, while expenses have increased due to COVID-19. The key question is whether occupancy is a near-term issue, or will persist post-COVID-19. The case for a return to normal is that skilled nursing care can be delayed, but not avoided, in most cases. For medical offices, the long-term concerns relate to telemedicine. The pandemic has led to a surge in the use of telemedicine, and some speculate it may drive a decline in the need for medical office space. However, increased access to screenings could lead to increased in-person visits for follow-up care. It remains too early to tell what effect telemedicine is having on health outcomes, much less on healthcare facilities.

- The uncertainty surrounding the multifamily residential property sector is less about a shift in demand and more about changing preferences. In particular, speculation is that COVID-19 will reduce demand for downtown living in coastal cities, home to many REIT apartment portfolios. Clearly the benefits of urban living, including access to restaurants and nightlife, are significantly diminished during the pandemic. However, broad evidence suggests that once consumers, especially young consumers, feel safe, they will quickly return to public spaces and in-person activities. The appeal of downtown living may be far more durable than some have speculated.

- Competing views about the future of office buildings and the prevalence of working from home are at play. Many have speculated the pandemic could lead to a permanent shift away from housing employees in offices for many companies. However, as the work-from-home trend nears the six-month mark, many organizations are starting to see productivity and collaboration suffer. Additionally, heightened concerns about social distancing and personal space could increase demand for office space, as employees are spaced farther from each other and protective barriers are put in place. This may ameliorate some of the reduced demand for office space created by work-from-home arrangements.

The pandemic has had differential short-term effects across commercial real estate property sectors, and will similarly have differential long-term effects. One of the keys to finding opportunities in the current real estate landscape is by differentiating between transitory and permanent changes in consumer behavior and the use of real estate.