Green bonds are playing a growing role in REIT fixed income strategy.

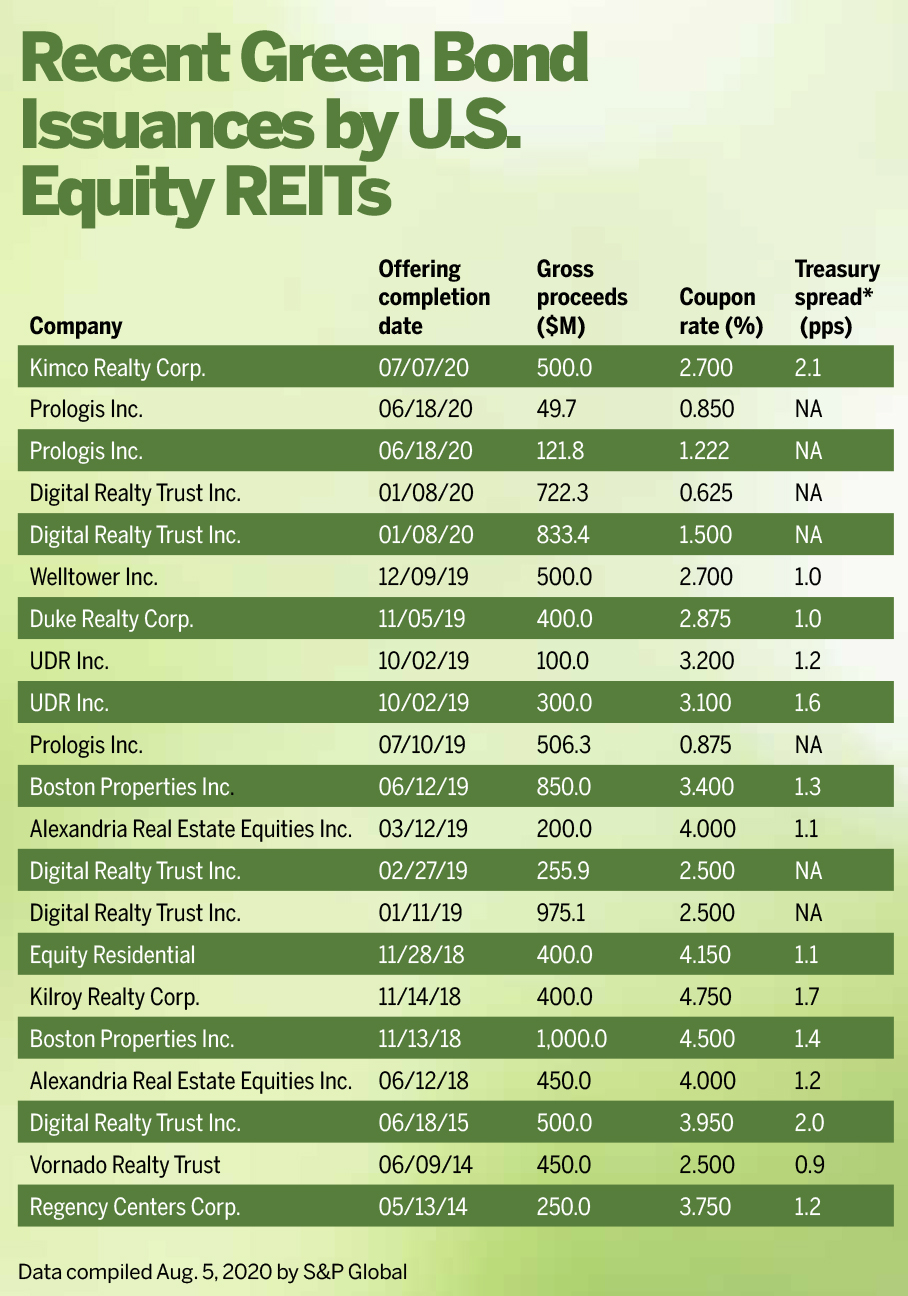

When Kimco Realty Corp. (NYSE: KIM) issued its first green bond this summer, it became the latest in a growing list of REITs to opt for the sustainable fixed income tool. While green bond issuance overall came under pressure in the first half of 2020, the heightened focus on ESG matters in response to COVID-19 should help maintain the long-term appeal of green bonds for REITs and their investors, experts say.

Indeed, Kimco’s recent offering underscores the level of interest in the green bond model, as the shopping center REIT chose to upsize its initial $300 million, 10-year green bond offering to $500 million.

David Bujnicki, Kimco senior vice president of investor relations and strategy, notes that ESG has increasingly become a key area of focus for many fixed income investors.

“Once they became comfortable with our broader commitment to ESG initiatives and how we planned to allocate the proceeds to green-related projects, it led to strong demand for the bonds,” Bujnicki says. “As a result, the order book grew very quickly, where it ultimately topped out at $1.8 billion.” Kimco was also able to tighten the pricing to a 2.7% coupon, he adds.

Ana Lai, a senior director at S&P Global Ratings, points to an increasing appetite for green bonds in the United States, especially in the last couple of years, although it continues to lag the level seen in Europe. Kimco’s increased offering was “good to see,” she notes.

“Investors are looking to increase their allocation to ESG-type instruments and the green bond market is certainly part of that,” Lai says.

Joshua Linder, credit analyst at APG Asset Management, says that because buildings generate a large portion of annual global greenhouse gas emissions, “the growth in green bond issuance coming from REITs is a promising development that we expect to continue because of the opportunity for meaningful impact.”

Pause, Then Pick-up

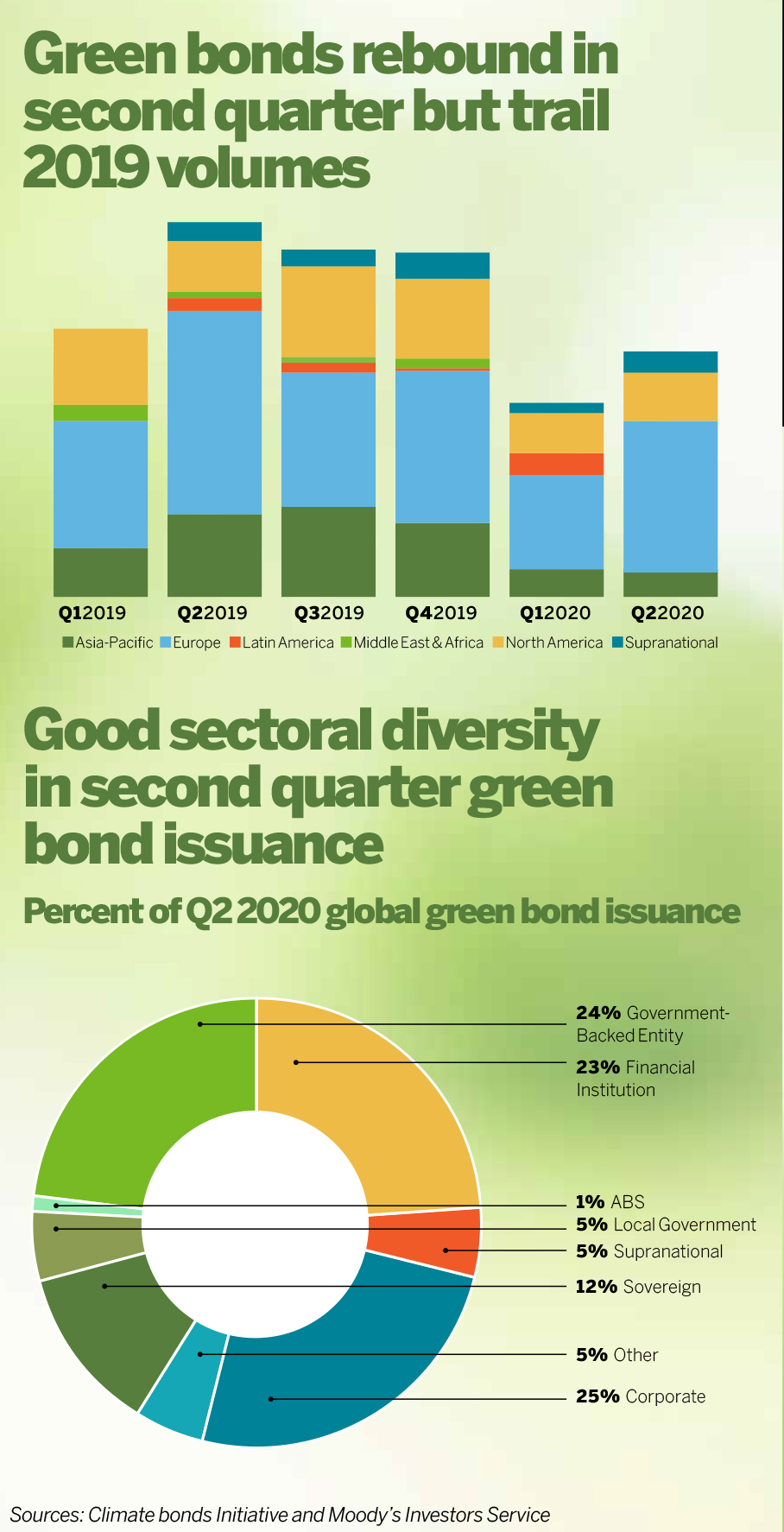

REITs have increased green bond issuance during the last few years, to the point where the industry is now one of the larger corporate sectors for issuance, in addition to utilities and banks, Linder says. Green bond issuance started the year strong but fell off in March and April as companies focused on their immediate liquidity needs caused by COVID-19; however, green bond volumes started picking back up in May and June, he adds.

REITs have increased green bond issuance during the last few years, to the point where the industry is now one of the larger corporate sectors for issuance, in addition to utilities and banks, Linder says. Green bond issuance started the year strong but fell off in March and April as companies focused on their immediate liquidity needs caused by COVID-19; however, green bond volumes started picking back up in May and June, he adds.

Marilyn Ceci, global head of ESG debt capital markets at J.P. Morgan, says the green bond market “paused for a moment” during the coronavirus crisis, but she expects the second half of 2020 to be robust.

“We had a very heavy pipeline pre-COVID; I do think the transactions that were delayed will eventually come back in the second half,” Ceci says.

On the whole, Ceci describes the green bond market as “booming—there’s no question about that and I expect it to continue. We’ve seen support from the sovereign market, and we’ve seen tremendous growth in U.S participation,” she says.

According to the Climate Bonds Initiative, global green bond issuance in 2020 is expected to total $350 billion, compared with $257.5 billion in 2019.

Meanwhile, Lai points out that while the Kimco offering did not offer any particular pricing advantage, REITs can benefit from tapping into an alternate investor base and source of capital, especially in a time of market volatility. Indeed, Kimco’s Bujnicki confirms that the REIT saw “a number of sustainability-focused fixed income investors that placed orders for our green bonds that were new names for us.”

James Magaldi, senior vice president, finance & capital markets, at Boston Properties, Inc. (NYSE: BXP), notes that green bond offerings are attractive to a broader pool of investors due to the positive environmental impacts and characteristics of the developments to which the REITs’ green bond proceeds are allocated. Boston Properties held two separate green bond offerings in 2018 and 2019, aggregating $1.85 billion.

“We share impact reporting to provide investors with metrics and equivalencies that quantify the environmental results. These metrics may include energy and water savings from efficiency measures and annually avoided carbon emissions from our eligible projects,” Magaldi says.

By labeling and identifying green assets, REITs do broaden their investor base, “without a doubt,” Ceci says. “If you continue to do that over time, it has to have an impact on your pricing. We have seen slightly better pricing—not on every transaction, but more and more over time,” she adds.

Importance of Transparency & Credibility

Linder also sees advantages for REITs to expand further into the ESG investment community, including the benefits that green bond issuance can bestow on a firm’s reputation.

“Many investors consider proper management of ESG risks and opportunities as another indicator of management quality, so issuing a well-structured green bond demonstrates to investors that the issuer is embedding material sustainability considerations into its long-term, strategic business planning,” he says.

When evaluating a green bond, the three things APG focuses on are transparency, accountability, and impact, Linder explains. “A lot of progress has been made regarding transparency of impact reporting, but there is still a high degree of variability in the quality, frequency, and approach of green bond impact reports, so we still see room for improvement,” he adds.

Ceci, who helped draft the Green Bond Principles (GBPs) that were published in January 2014 by a consortium of leading banks and have become commonly accepted guidelines of market best practices, adds that some green bonds are structured with more transparency than others. The majority of green bonds in the REIT space are using and referencing well-established certification schemes, she says.

Ceci points out that the European Union is working on creating a green taxonomy as well as an EU green bond standard, green benchmarks, and requirements for green disclosure for issuers. She does not expect the U.S. to follow this approach in the near term.

“Those of us who worked on the GBPs feel very strongly about allowing the market to grow and expand without prescriptive definitions. Investors certainly need the information, but they can make their own informed decisions on what’s green enough for their own portfolio. The market can be transparent and credible even without regulations,” Ceci says.

“Those of us who worked on the GBPs feel very strongly about allowing the market to grow and expand without prescriptive definitions. Investors certainly need the information, but they can make their own informed decisions on what’s green enough for their own portfolio. The market can be transparent and credible even without regulations,” Ceci says.

The Rise of Social Bonds

While green bonds continue to account for the bulk of the sustainable debt market, experts also say the pandemic has been a boon for social bond issuance.

“The S of ESG is equally as important to investors as the E and we fully expect demand for social bonds to grow. The intent of impact investing has always been to generate positive social or environmental impact, alongside financial returns,” Magaldi says.

COVID-related social bond issuance has been led by development banks and other government and semi-government agencies, but a few corporate issuers have also come to the market, according to Linder.

“Given the scale of the global pandemic, we expect more funding will be required to help combat its negative impact, which may come in the form of financing health care solutions or assisting in the economic recovery,” Linder says.

APG is still pushing for green bond issuance alongside COVID-themed social bonds. “We expect demand for both should remain strong. It’s possible that we may see issuers combine COVID-related social expenses with other green initiatives in a sustainable bond program,” he adds.

Although green bonds are the natural starting points for REITs, given their environmental impact, Linder says there is no underlying reason why REITs couldn’t issue a social or sustainable bond, COVID-related or otherwise. “The key will be around properly defining eligible use-of-proceeds and developing impact metrics that are truly impactful and go beyond the status quo,” he says.

In early May, APG published a guidance document outlining expectations for how corporate issuers can incorporate COVID response efforts into a social or sustainable bond program, with the aim of encouraging greater issuance to address the pandemic, while maintaining the integrity of the market.

Ceci, meanwhile, does not see social bonds as impinging on the growth of green bonds, given the “massive spend” around climate issues.

“I still expect the green bond market to be eight times the size of the social bond market. There was a very obvious large spend on the social side as a result of COVID, but I’m not too sure that spend is there all the time,” Ceci says.

Read more from September/October issue of REIT magazine, available now in an interactive PDF.