Public REITs were among the first markets to feel the ramifications of the Federal Reserve’s aggressive rate-hiking cycle. Now, as the pendulum begins to swing back the other way, the sector is positioned to reap the benefits of outperformance.

The Federal Reserve voted Sept.18 to lower the target range for the federal funds rate by a half percentage point to 4.75%—5.0%. Policymakers see the Fed's benchmark rate falling by another half a percentage point by the end of 2024, another full percentage point in 2025, and by half a percentage point in 2026.

Prior to the Sept. 18 announcement, the prospect of rate cuts had already started to impact market expectations and pricing. Since April, the 10-year Treasury yield has declined about 100 basis points to hover at around 3.65% as of Sept. 18. “The fact that short rates will go lower is well established, but the market will look for more clarity on the path and duration of future cuts beyond the opening salvo,” says Michael Knott, managing director and head of U.S. REIT Research at Green Street. Now that inflation appears to be in line with Fed targets, the path of cuts going forward will likely be influenced more by incoming economic and employment data.

Real estate is obviously a capital-intensive sector, but the market concern related to cost of capital increases has been somewhat unfair, adds Matthew Sgrizzi, chief investment officer of LaSalle Global Solutions. Tightening liquidity among banks, for example, has actually been an opportunity for REITs because they have had good access to the bond market and they went into this higher rate cycle with well-termed debt and some of the lowest leverage ever, he says.

“I think we’re seeing market sentiment towards real estate turn towards a more positive stance, and that’s being supported by this change in Fed policy,” Sgrizzi says. Rate easing cycles are very supportive for REITs. There’s every reason to expect that to play out this time as well, and the market is just starting to see the early days of that beginning to come through. However, the track ahead is long and it could be a multi-year catch-up for REITs compared to broader equities, he adds.

Welcome Relief for Real Estate

Warranted or not, REITs have felt the pain of the higher-for-longer cycle. “Listed REITs are always at the tip of the spear. They took it on the chin in 2022, earlier than the private real estate market, and now they’ve been recovering much quicker than the private real estate market,” says Jason Yablon, head of listed real estate at Cohen & Steers.

The private REIT market is still seeing NAV cuts to their appraisal values because it takes longer for appraisal values to catch up to the real-world values, whereas the listed REIT market is always re-triangulating to forward expectations of how investors think things should be valued, he says.

During the recent Fed hiking cycle, REITs saw their earnings multiple de-rate more than any other equity sector. Fundamentals have remained fairly robust, with REIT earnings growing by a cumulative 18% at the same time as their share prices declined by 22%, according to Janus Henderson Investors. That underperformance over the last couple of years is largely explained by the higher interest rate environment.

“When rates are falling and the market expectation for future rates is flat to down, we believe it’s reasonable to expect REITs to reverse this trend and outperform other equity sectors,” says Greg Kuhl, portfolio manager at Janus Henderson Investors.

The tide on investor sentiment began turning as the Fed neared its 2% inflation target. “In our view, the benign May inflation data was the beginning of a shift in market expectations for the future path of interest rates to include near-term cuts,” Kuhl says.

Since this data was released in early June, REITs have been the best-performing GICS sector within the S&P 500, delivering a total return of 16% compared to the overall S&P500 at 1%. “When a rate cutting cycle is commenced, we would not be surprised to see a continuation of REIT outperformance, despite some expectation of lower rates already being evident in the market,” he says.

Pivot to Outperform

The recent period of inflation and higher interest rates resulted in lower growth expectations, which was a big headwind for listed REITs. Investors pulled back from REITs as interest rates rose and property values corrected. According to Yablon, real estate has not been this “under-owned” since the global financial crisis.

The best scenario for REITs is one where interest rates are declining, and the economy is moving towards a soft landing. If financing costs for real estate are improving while the cash flow at a property is still doing reasonably well, then the value of that property should rise. Although there’s still healthy debate around the trajectory of growth expectations, it's a much better backdrop for listed REITs and values are still cheap relative to the broader equity market.

“Moving into this new regime is a very important change, and this is a change that is not yet fully reflected in the listed REIT market,” Yablon adds. “I say that because REITs are still under-owned. So, I think what you’re going to begin to see is an increased allocation to listed REITs from a portfolio allocation standpoint because we fulfill a particular niche right now.”

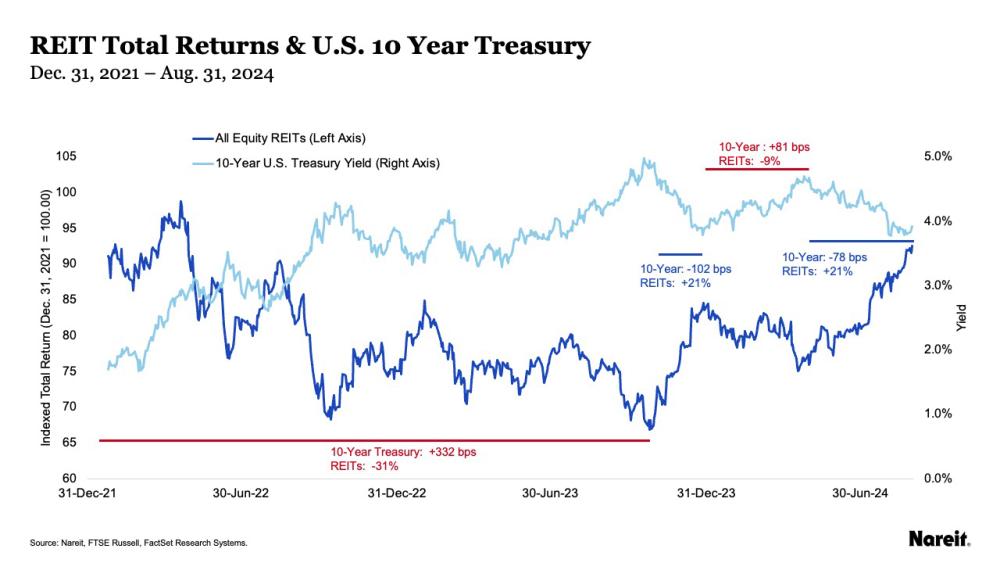

The REIT rally is already showing up in performance data. “Starting in 2022, what you'll find is that there's been an inverse relationship in the performance of REITs and the movements in 10-year Treasury yields,” says Ed Pierzak, senior vice president of research at Nareit. Typically, as 10-year Treasury yields decline, REIT total returns tend to rise. Total returns for the FTSE Nareit All Equity Index during July and August were quite strong during that same period, up 7.2% in July and another 5.6% in August.

Ready to Play Offense

In the near term, REITs likely will be subject to day-to-day share-price volatility as the public equity market digests and reassesses changing probabilities on the path for lower rates, along with economic data.

Looking at the medium and long-term horizon, there are two important impacts of lower rates on REITs, both of which should drive future earnings and dividends higher, Kuhl says. One is lower refinancing costs, which will lead to greater than previously expected earnings growth. Two is improved cost of debt and equity capital, which will allow public REITs to go on “offense” and grow externally by acquiring real estate at accretive prices from private owners facing balance sheet pressure.

Looking at the broader commercial real estate market, challenges associated with the higher for longer rate environment were exacerbated by the regional banking crisis, which contributed to tighter liquidity. At the same time, there were negative headlines around the mountain of commercial real estate debt maturities and distressed loans in the office sector in particular. As a result, there has been a sharp decline in transaction activity for the past two years due to pricing uncertainty and fears about the economy.

Rate cuts likely will signal a bottoming on values, and REITs are in a good position to take advantage of buying opportunities. “One of the things that we have presented all along is that REITs have really been in a great position during the ups and downs of the cycle, and a lot of that stems from their balance sheets,” says Pierzak. The latest data from the Nareit Total REIT Industry Tracker Series (T-Tracker®) report shows that REITs continue to have healthy balance sheets. Highlights for listed REITs include:

- Among total debt, the majority was unsecured at 79.2% and 90.8% of total debt was fixed rate.

- Leverage ratios were low with debt-to-market assets at 34.1%.

- Weighted average term to maturity of REIT debt was 6.4 years.

- Weighted average interest rate on total debt was 4.1%.

“The two biggest things when you peel the onion back when looking at the composition of REIT balance sheets is that they are very focused on fixed-rate debt as well as unsecured debt,” Pierzak says. In addition, leverage ratios that are just under 35% are very low levels that are akin to a core or core plus strategy, and the weighted average maturities are out more than six years. “So even though we went into this environment of higher interest rates, REITs really didn't have a lot of exposure at all to that,” he adds.

Even in the tougher capital environment, REITs have continued to access capital at very competitive rates. During the second quarter of this year, REITs issued over $12 billion of unsecured debt at an average cost of about 4.5%. “REITs have easy and efficient access to capital that is cost-advantaged relative to the private side of the market. So, as we start to see more transactions, we may very well see REITs becoming more active buyers,” Pierzak says.

Another byproduct of the higher-rate environment is that it has constrained construction activity. There is limited development in many sectors that will impact supply beginning in 2026 and 2027, which will be a positive for commercial real estate fundamentals.

“I think the setup for the REIT market is really good today. There have been a lot of headwinds that the market has been concerned about for REITs, and I think some of that's unjustified,” Sgrizzi says. “We now have this easing cycle that's unfolding for a capital-intensive asset class that can really be a tailwind for our sector. We're starting to see that play out, but clearly, that’s still in the very early stages.”